(This project was done as part of the post-graduation program in UX design at IDC School of Design, IIT Bombay)

Problem statement

Managing finances in a digital age for Indian households

Context

- Smartphone penetration in India is high, with over half of families owning one.

- Demonetization, UPI adoption, and post-pandemic hygiene concerns have significantly increased digital payments.

- Small businesses are readily accepting digital transactions.

Challenge

- The shift towards digital payments creates “invisible money,” making it difficult for families to visualize and track their spending.

- Traditional cash-based budgeting methods become ineffective with intangible transactions.

Impact

- Difficulty in managing household finances effectively.

- Potential for overspending or poor budgeting decisions due to lack of visibility.

- Reduced ability to save and plan for the future.

Current Solutions (Gap)

- Existing payment apps and expense trackers lack integration for holistic financial management.

- These tools primarily focus on spending tracking, neglecting saving and budgeting functionalities.

Opportunity

- Develop an innovative app that seamlessly combines spending, saving, and budgeting tools for Indian families.

- Leverage the data generated by digital transactions to provide real-time insights and improve financial awareness.

- Empower families to take control of their finances and achieve their financial goals.

The team

During my PG program, I honed my UX design skills by collaborating with a team of 4 designers across India on a 6-month project.

We wore all hats – researchers, information architects, interaction designers, and visual designers.

User group

We targeted middle-class families (both upper and lower) in urban India. This demographic:

- Balances income and spending: We focused on those who actively manage their finances.

- Adopts digital payments: They’re comfortable with the technology for user research.

- Has smartphone access: Urban areas have higher smartphone penetration.

Contextual inquiry

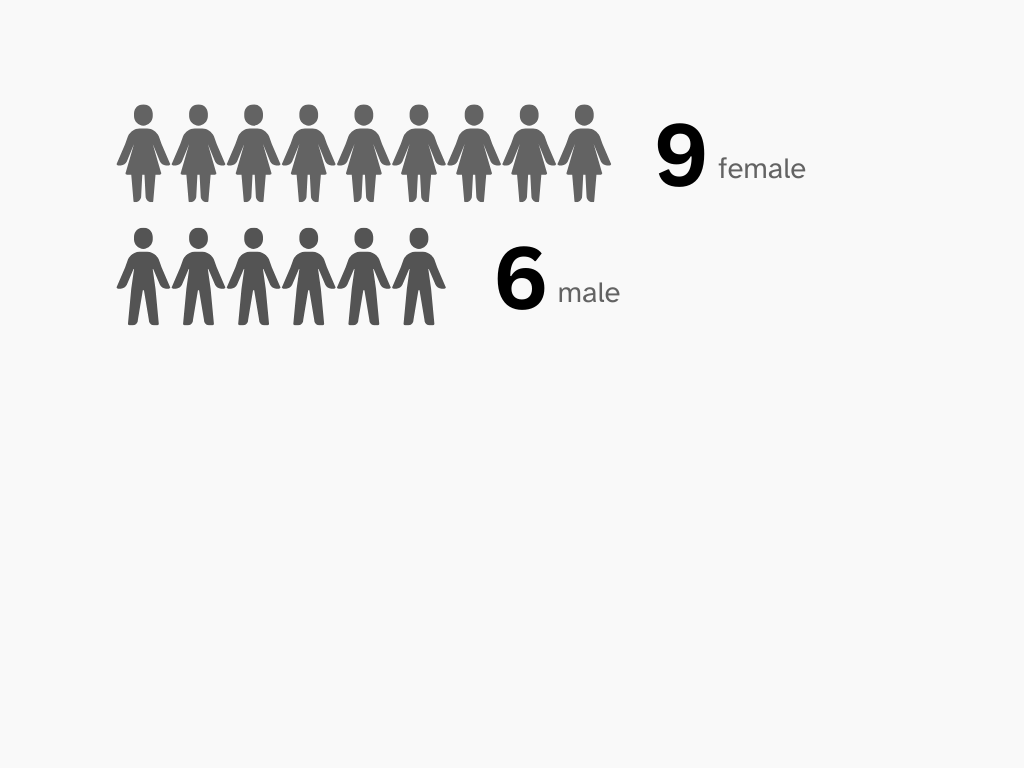

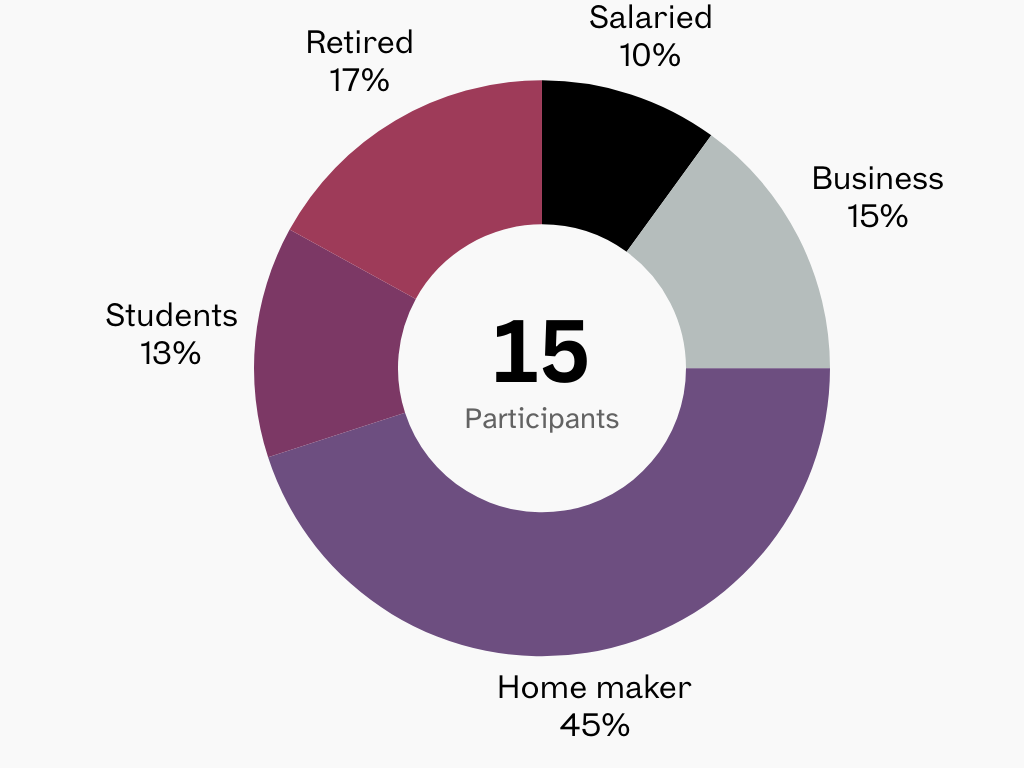

For a comprehensive understanding, we interviewed 15 participants from 9 Indian states, encompassing a variety of urban and suburban backgrounds.

Research goal

- How do people in urban Indian middle-class families track and analyze their household expenses?

- What challenges do they currently face?

- What are their spending vs. saving habits?

- What methods do they use to keep a track of their expenses?

- Are these methods effective?

- How have these methods evolved over time?

- What role does family dynamics play in the process?

- How do family members collaborate?

- And how is the work divided?

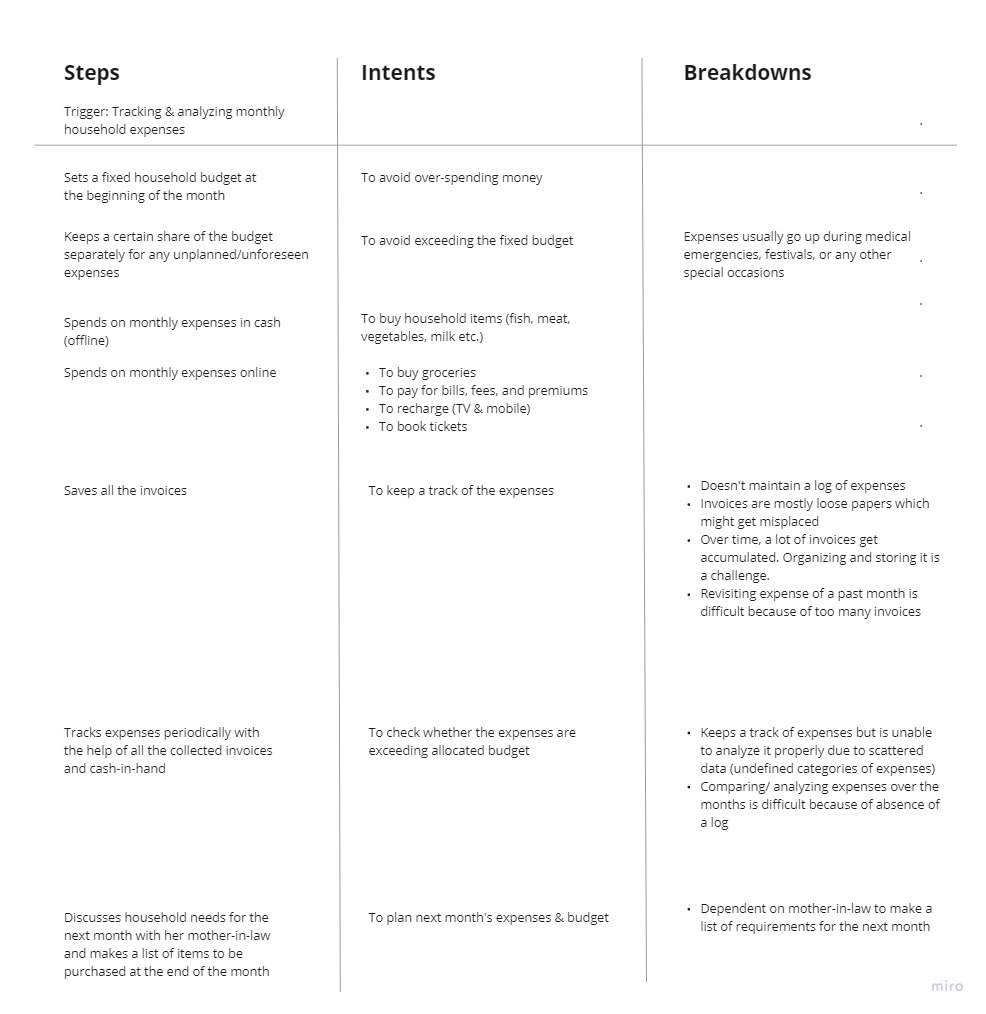

Interpretation and ‘work models – a language for seeing work’

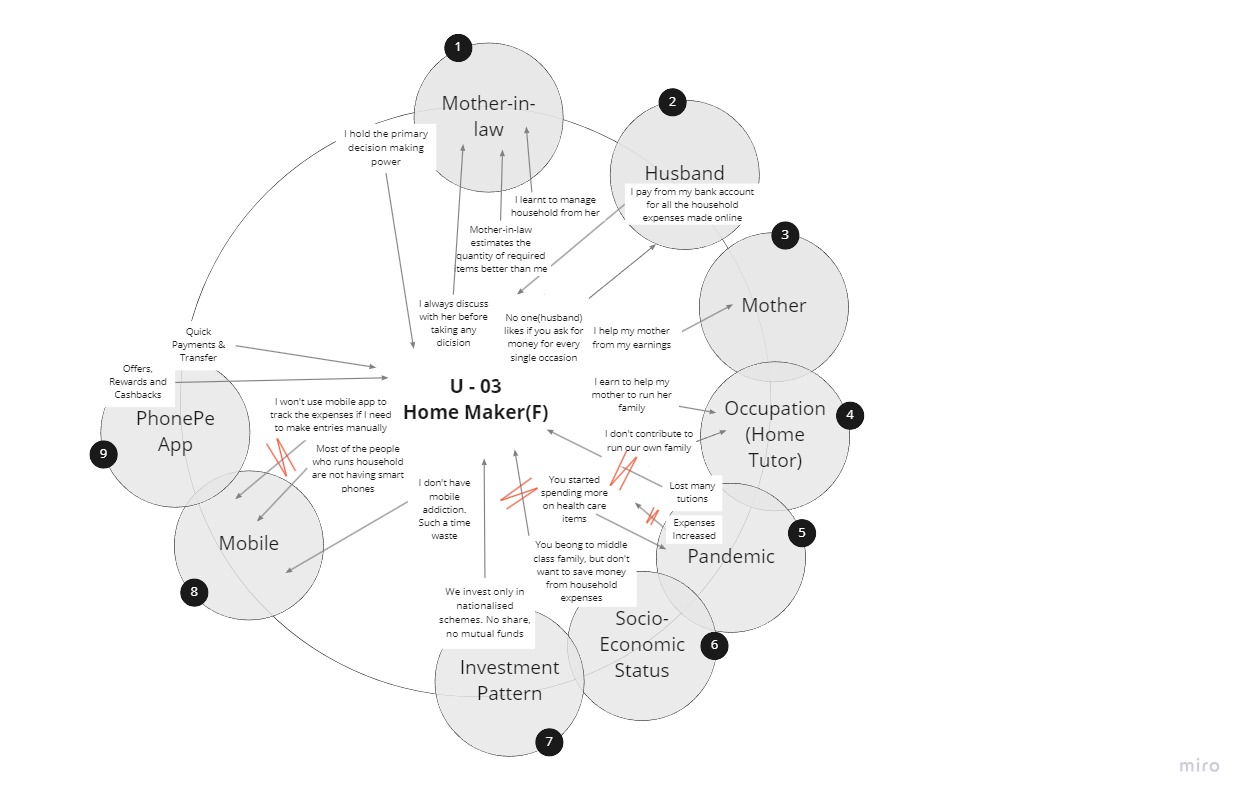

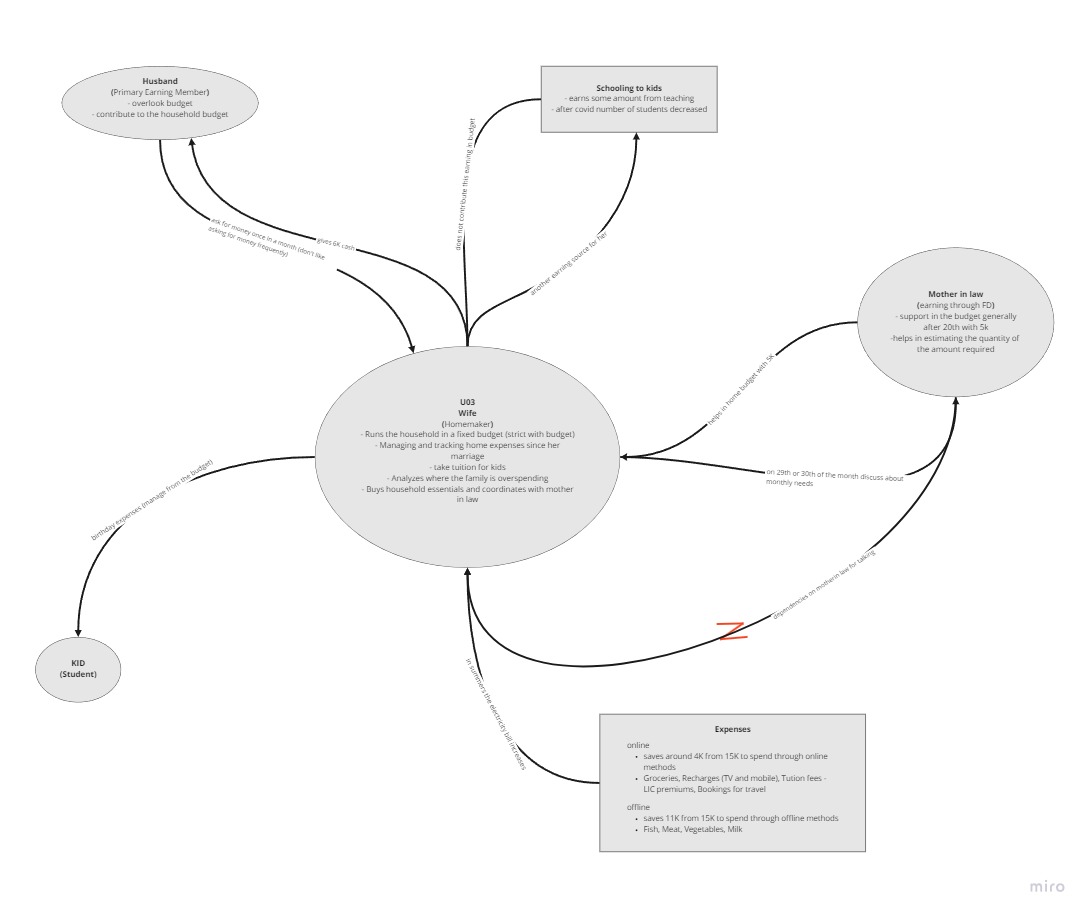

Following contextual inquiries, we developed cultural, flow, artifact, and sequence models to analyze user interactions. These models provided valuable insights into user behavior, interpersonal dynamics, challenges with physical materials (diaries, invoices), and the workflow for managing monthly household expenses.

Insights

Through Affinity mapping, we distilled the data into meaningful clusters and categories.

1. Users have different accounting approaches.

One of the key findings from our affinity was that users have different accounting behaviors.

- Conscious spenders – “Instead of tracking my expenses, I would rather spend cautiously.”

- Fixed budgeters – “I fix my monthly budget to avoid overspending”.

- Free spenders – “I don’t plan before spending because I believe, you only live once.“

- Post analyzers – “I spend first and analyze later to find unnecessary expenses.”

When these different spending behaviours and accounting approaches exist within the same family, it may create a conflict.

2. Striking a balance between transparency & privacy among family members is a challenge.

The above point is a big challenge in home accounting. While users wanted the process to be more transparent so that all the family members can seamlessly coordinate with each other and manage their expenses together, they did not seem comfortable with sharing all their financial information with their family. This especially holds in families where there are multiple earning members with a generation gap.

“If your parents can see your expenses in real-time, you wouldn’t be comfortable. You don’t want to involve them in day-to-day transactions, like disclosing exact salaries and how much are you spending where.”

– User 1 (Working professional brought up in a conservative household, but holds modern values)

3. Communication gap & unequal distribution of work within a family is a challenge

We also found that unequal distribution of work and communication gap within the family members makes home accounting inefficient and challenging.

“I have to remind my husband time and again to pay the electricity bill on time.”

– User 2 (Homemaker who doesn’t like constant nagging)

4. Collaboration makes home accounting more efficient. Young members bring in their digital expertise while elders bring in their years of experience.

Through our contextual inquiry, we realized that the process of home accounting is more efficient in families where family members bring in their expertise. Young members in the family often bring in a fresh perspective and teach elders new ways of doing things like helping with digital payments or finding cost-effective ways of shopping. On the other hand, elder members bring in their years of experience, discipline, and encourage savings in the household.

“My mother has a fixed fruit ‘waale bhaiya’ (vendor) who she buys fruits from because she thinks he’s more reliable. But there are much more affordable options for buying fruits like Instamart, Big Basket etc. that she wasn’t aware of until I told her about it.”

– User 7 (25-year-old daughter)

5. There are inefficiencies in the current accounting processes

- Lack of an integrated platform for recording hybrid (online & offline) expenses – In most cases, cash payments & digital payments are recorded separately, which makes keeping a track of expenses challenging

- Current data entry methods are time consuming – Users use different methods to track their expenses and each of these methods have their own set of challenges.

- Difficulty in analyzing expenses – Users face difficulty in analyzing expenses due to scattered data and undefined categories.

6. Financial Literacy among the youngsters from their early ages is important

Another interesting insight from our finding was that most of the young parents that we interviewed understand the importance of financial literacy and want their young children to learn the “value of money” early on in their life. And they feel taking part in home accounting is a great starting point.

“Managing money, salary negotiations etc. is never taught in schools in India. Financial literacy is a big issue”

– User 1 (IT professional, whose cousin is currently facing the same problem)

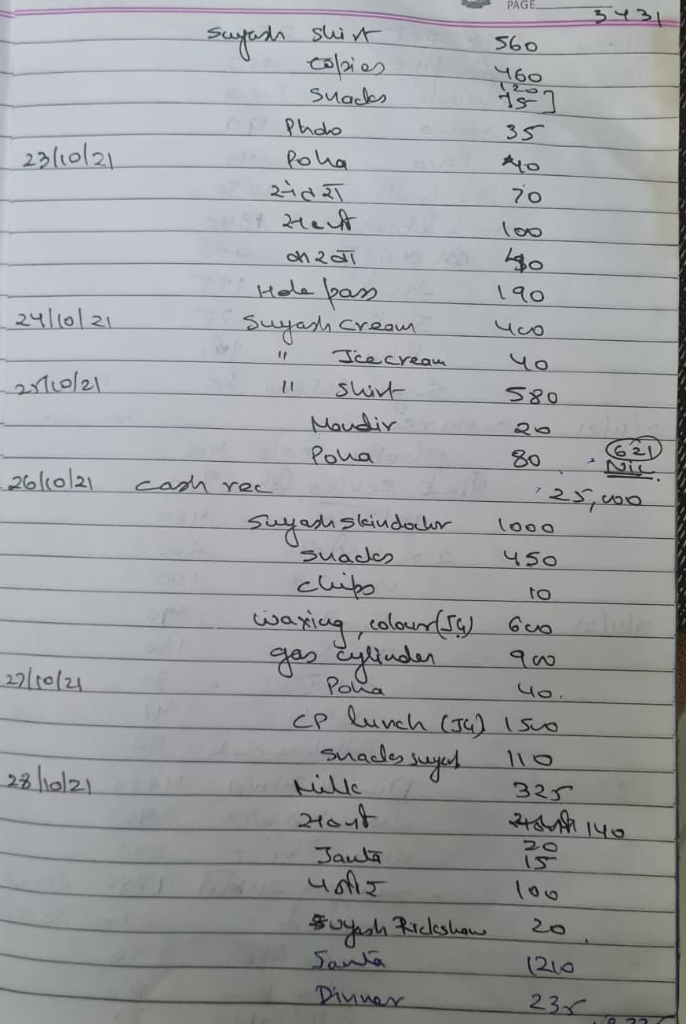

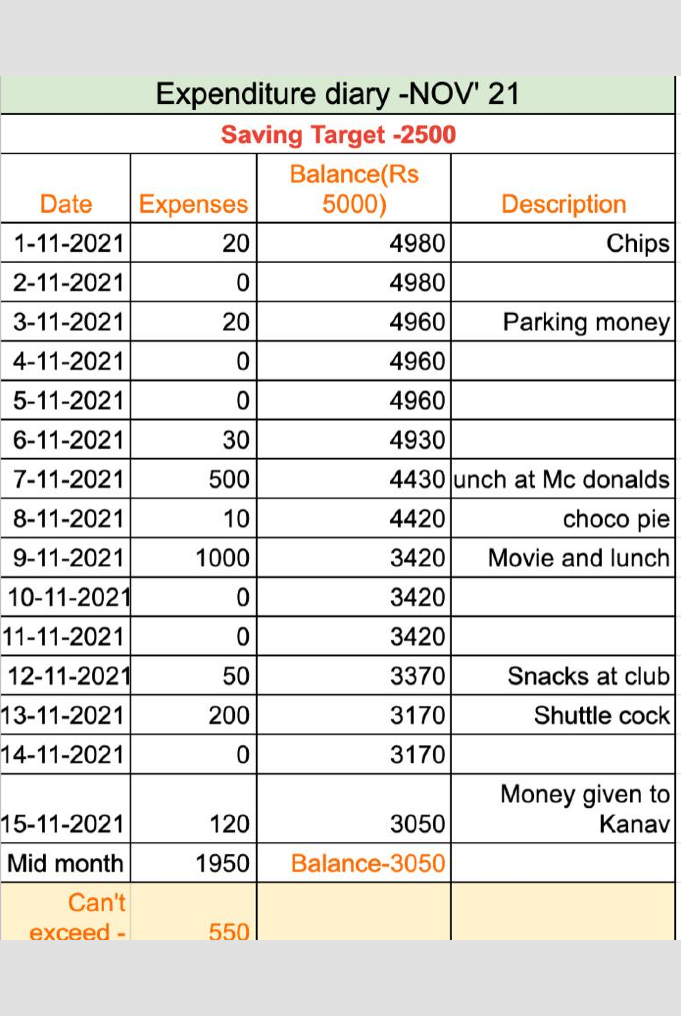

Issues discovered after analyzing the artefacts collected from different users

Saving invoices

- Loose papers might get misplaced.

- Over time, a lot invoices get accumulated. Organizing and storing is a challenge.

- Revisiting expenses from past month is difficult.

Recording in a diary

- Categorizing of expenses under buckets is difficult.

- Analysis is a challenge.

- Physical constraints.

Tracking through an app

- Absence of integration from other payment apps.

- Recording expenses is not automated.

- Increased screen time.

Maintaining excel

- Absence of a pre-existing template makes data categorization difficult.

- Absence of integration from other payment apps.

- Recording expenses is not automated.

Personas & scenarios

Through the lens of personas and their scenarios, we demonstrated how our solution would deliver tangible benefits and solve real-world challenges for our users.

Mrs. Kusum Khanna

Home maker, 50 yrs, Delhi

Novice smartphone user

A diligent homemaker, she maintains a meticulous record of household expenses to effectively manage her family’s finances.

Goals & Motivations

- Get a clear picture of where her money is going

- Reduce communication gaps & make home accounting more transparent

- Improve collaboration within the family and make kids more financially aware

Problems & Challenges

- She often forgets to record petty expenses in her diary

- She has to keep reminding her husband & kids to do household chores like order grocery/ pay electricity bills

- She doesn’t have the time to analyze expenses to find where the family is overspending.

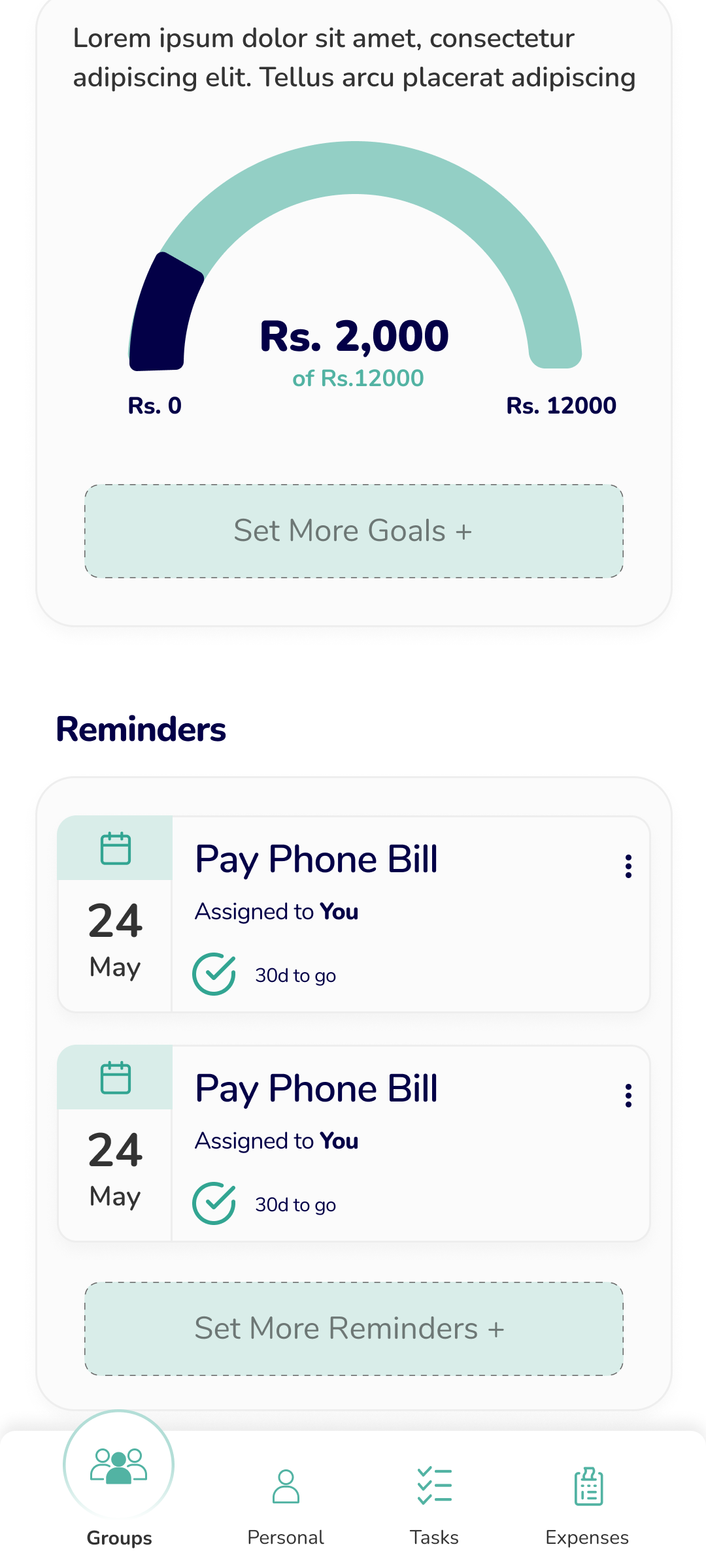

How Finjam (our solution) fits into the life of Mrs. Kusum Khanna

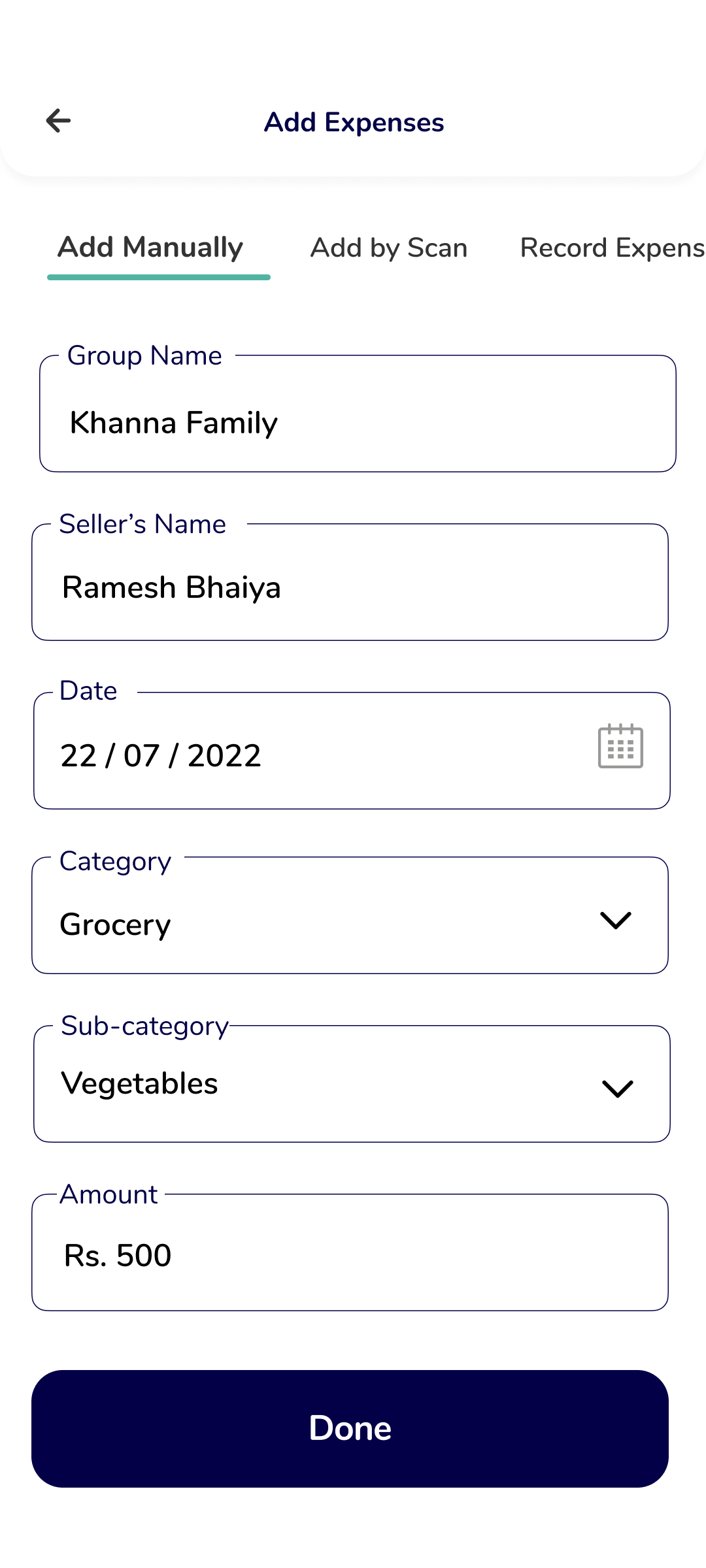

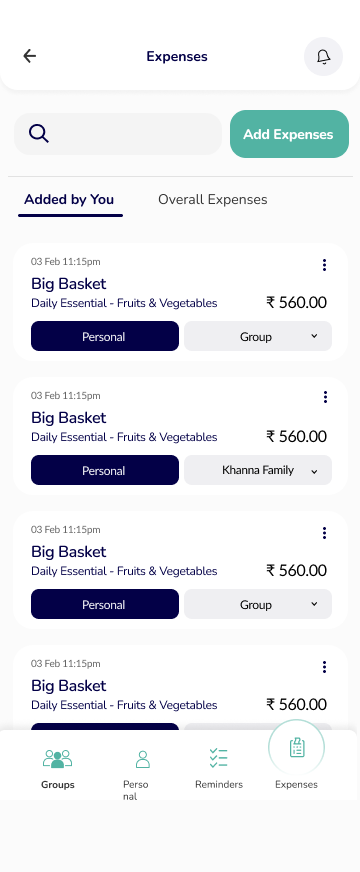

Scenario 1: Adding Expenses

Every morning Mrs. Khanna goes to the flea market to buy fresh fruits and vegetables. She pays the vendor in cash.

Step 1:

She opens Finjam and tap “Add Expenses”.

Step 2:

She quickly adds these expenses to the household account so that she doesn’t forget to add it later.

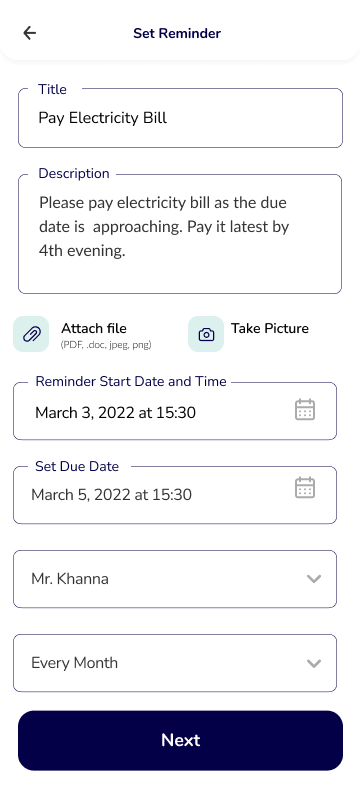

Scenario 2: Setting reminder for family member

Mrs. Khanna’s husband often forgets to pay the electricity bill on time. She uses Finjam to set a reminder for him and the app reminds him to make sure he doesn’t miss the deadline (due date for the bill).

Step 1:

Mrs. Khanna taps on “Set More Reminders” from the home screen.

Step 2:

She creates reminder for Mr. Khanna to pay the bill on time.

Scenario 3: Control access

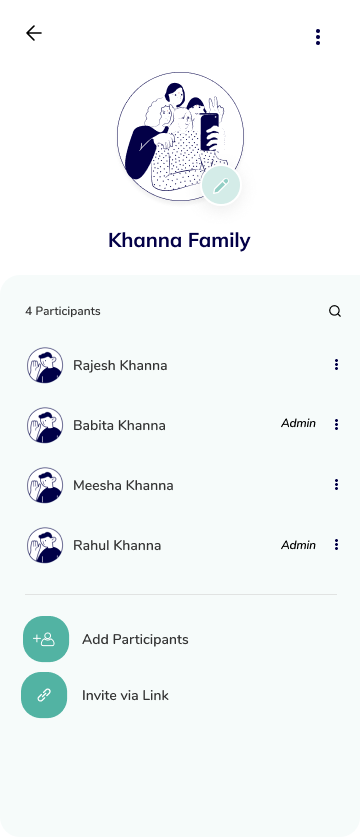

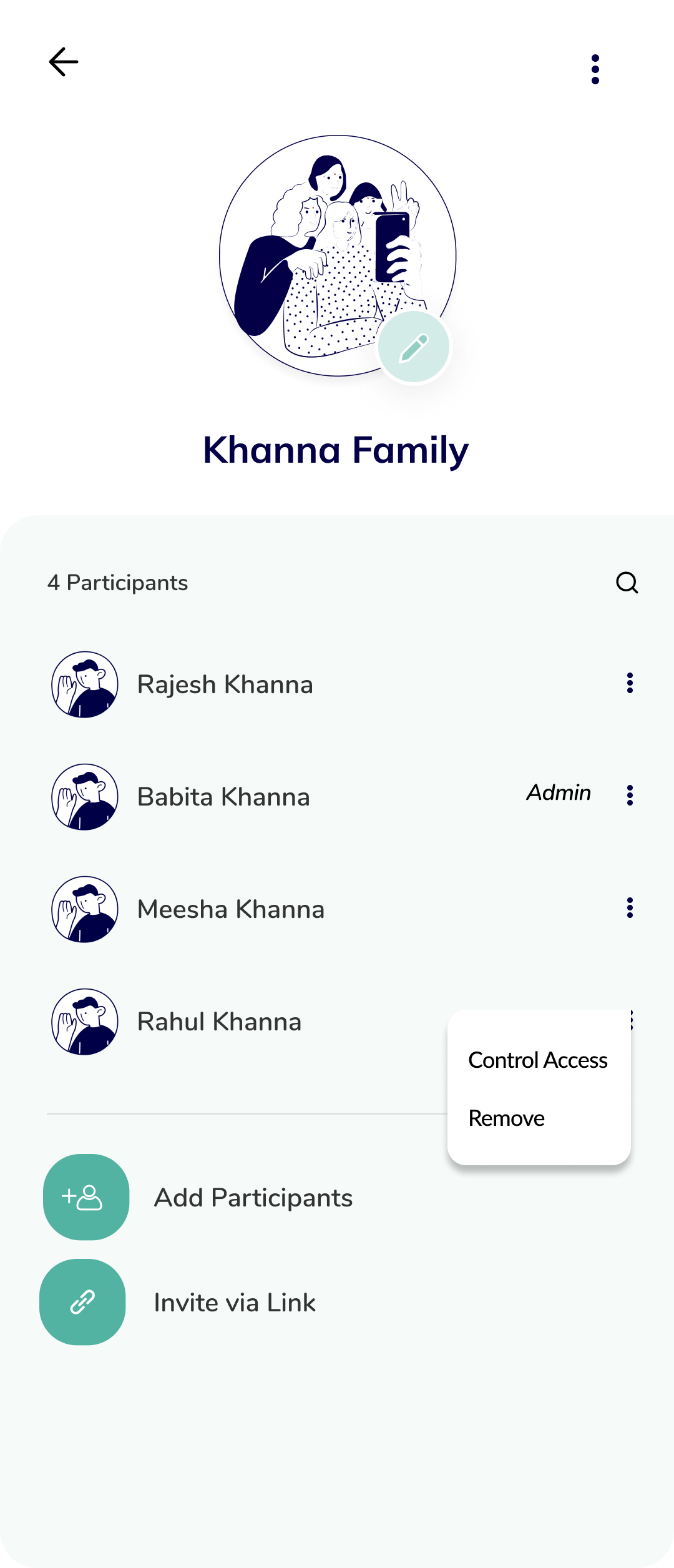

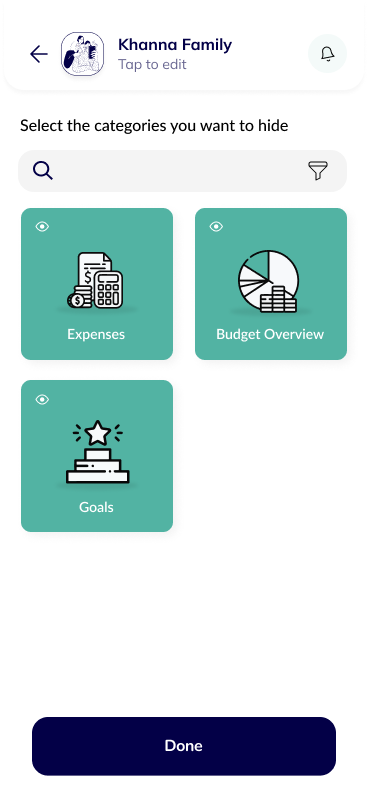

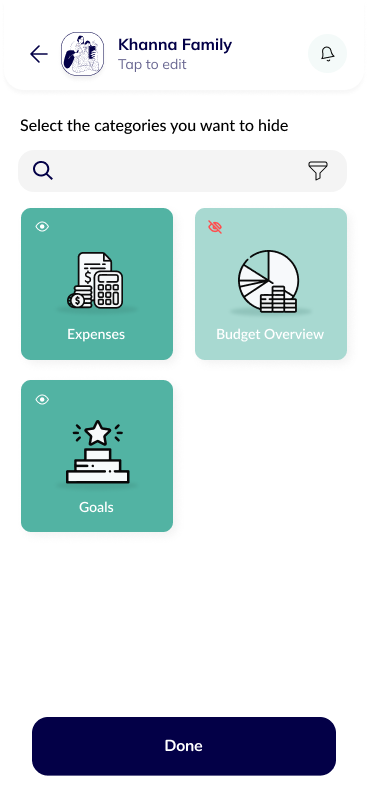

Mrs. Khanna always wanted her kids to understand the value of money. She uses this app to involve her son Rahul in the day-to-day process of home accounting so that he learns how to spend money. She also has an option to control how much of access does she want him to have.

Mrs. Khanna reaches family profile page and tap on ellipsis menu(more) right after Rahul’s profile. She taps on control access.

She then turns off access for a particular category (budget overview) for Rahul’s profile.

Personas & scenarios

Mr. Rakesh Khanna

Businessman, 55 yrs, Delhi

Novice smartphone user

He is a business owner and the primary financial provider for his family.

Goals & Motivations

- To get a better understanding of household expenses

- To make informed investment decisions & identify saving opportunities

- To be able to meet deadlines & make timely payments

- To develop healthy spending habits among kids

Problems & Challenges

- He has a hectic work-life & doesn’t get time to look into home accounts

- He often forgets to pay power/gas bills on time

How Finjam (our solution) fits into the life of Mr. Rakesh Khanna

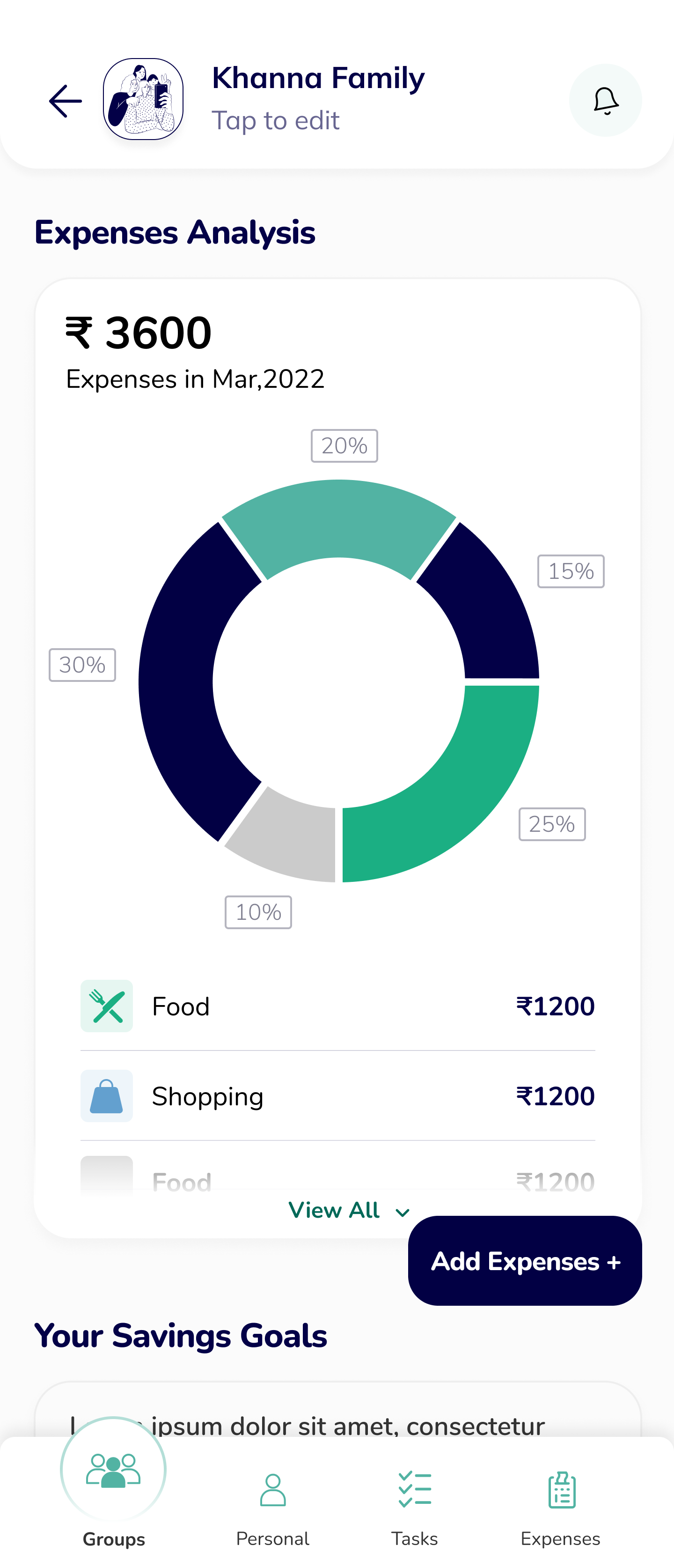

Scenario 4: Expenses analysis

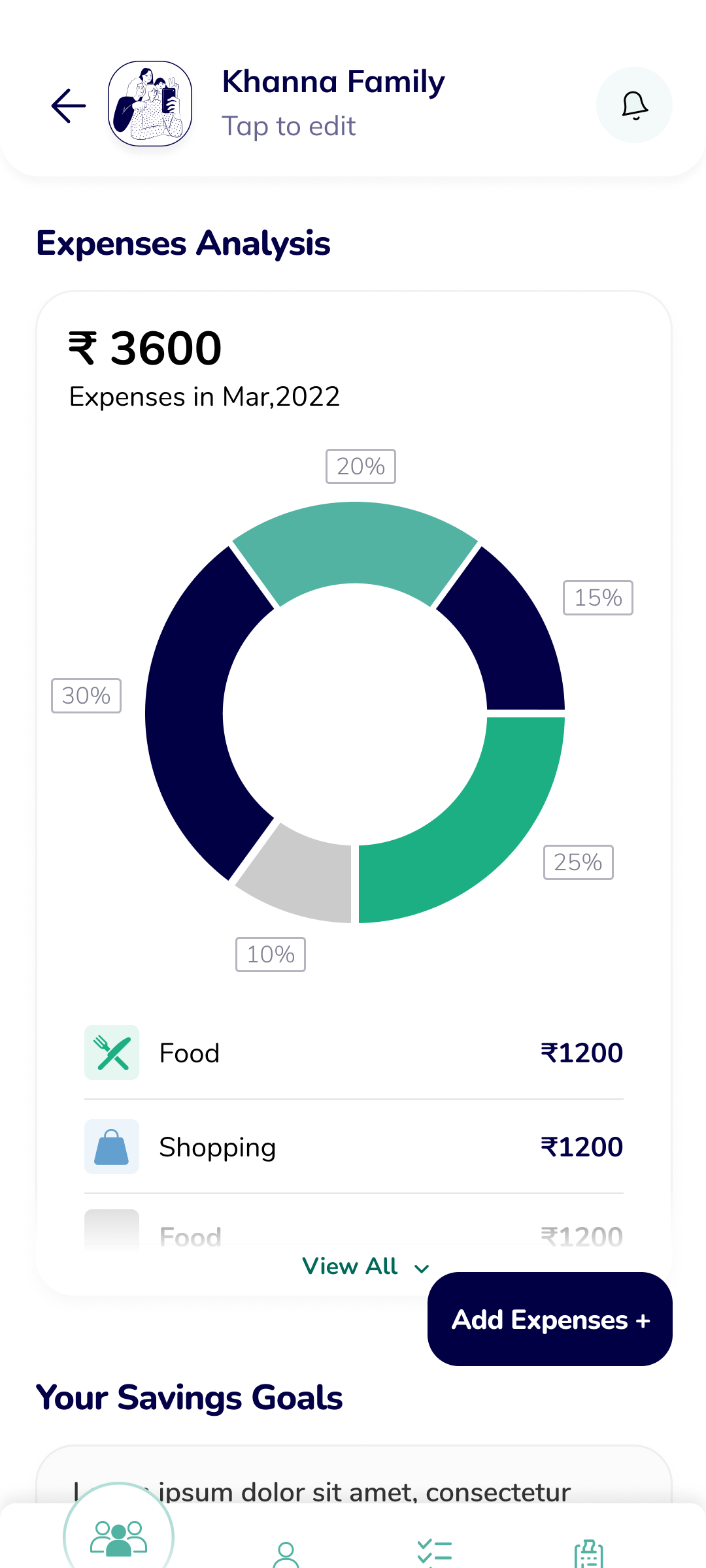

Amidst his busy work life Mr. Khanna uses Finjam to quickly go through the household expenses and get a detailed and in-depth insight into it.

Mr. Khanna checks the home screen to have a look on the transactions and their patterns.

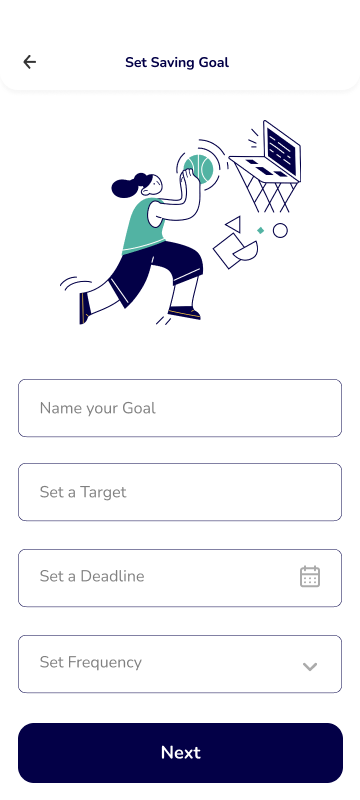

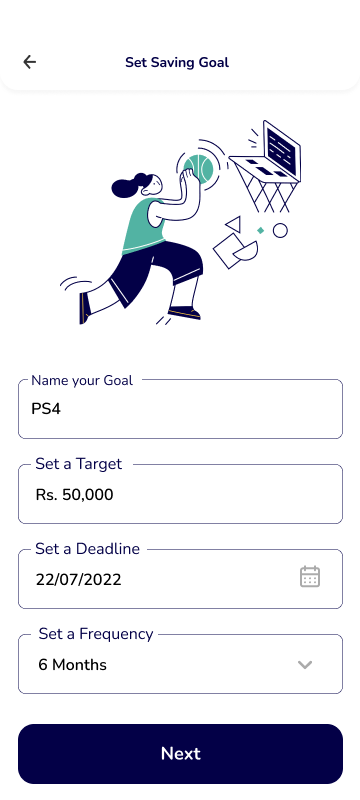

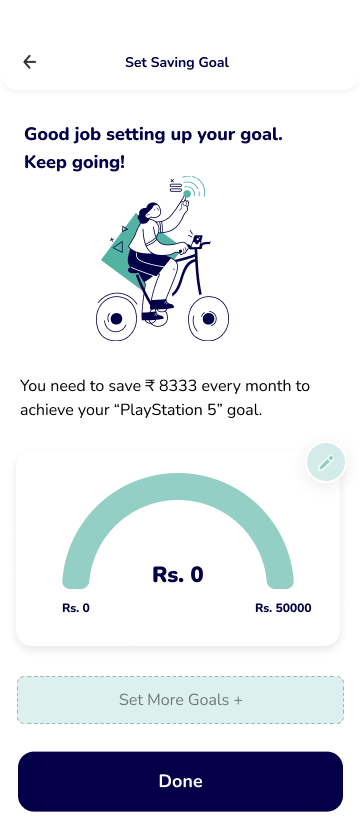

Scenario 5: Setting a goal

Mr. Khanna is planning to buy a new smart TV for his home in next three months. He uses Finjam to set a goal to save Rs. 50000 so that the entire family plan it together and make it happen.

Mr. Khanna taps on “Set a goal” from home screen and fills up the details eventually for setting up goals

Personas & scenarios

Ms. Meesha Khanna

Sales Executive, 25 yrs, Delhi

Expert smartphone user

With a passion for retail therapy and a love for Korean dramas, she’s recently entered the workforce and continues to live at home with her family.

Goals & Motivations

- Become financially independent

- Keep a track on over-spendings

- Plan her expenses better

- Invest & grow her money

- Make better financial decisions

- Contribute to household income

Problems & Challenges

- Struggles with monitoring her expenses

- Tends to overspend

- Doesn’t get time to look into her finances because of a busy work-life

How Finjam (our solution) fits into the life of Meesha

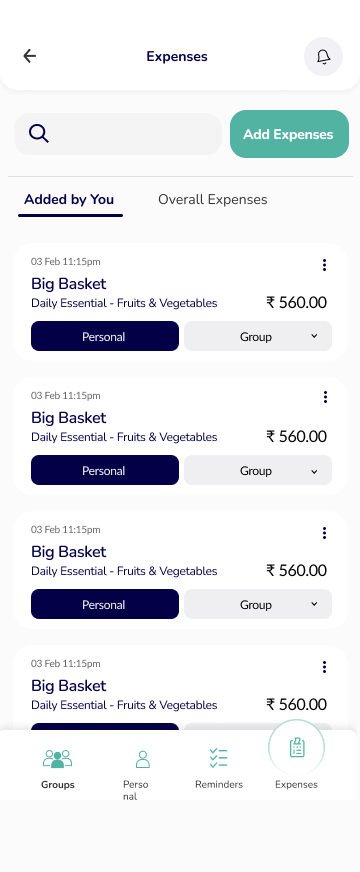

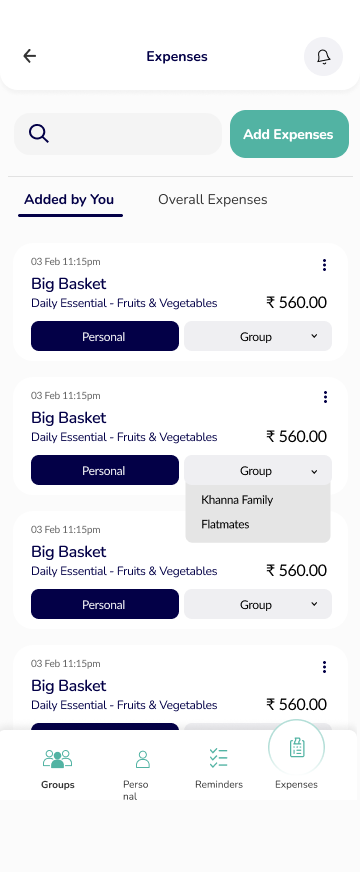

Scenario 6: Categorizing expenses into personal & group

Meesha loves online shopping and often tends to overspend. She uses Finjam to keep a track of her personal expenses as well as the home expenses so that she gets an overall picture of her total spendings. This also allows her to keep her personal expenses private from the entire family.

Meesha segregates her spending into her own as well as household by going to her expenses screen.

Design evaluation

Key questions

- Does our app make tracking & analyzing home expenses simple?

- For a novice user, how easy is it to use the application without any help?

- Are both young & elder members in the family who have different levels of digital literacy comfortable with using the app?

- Is the app improving collaboration among family members?

- Is the app giving the family a clear picture of where their money is going?

Methodology: Heuristic Evaluation :: by 5 usability experts

Our solution (UI) was shared with 5 different usability experts for conducting evaluation based on Jakob Nielsen’s 10 usability heuristics. Following issues were found –

- Consistency & navigational clarity

- Same features are named differently

- Look & feel of buttons is inconsistent

- Match between system & the real world

- Issues in user flows

- Context of features is missing

- User control & freedom

- Confusion between primary and secondary actions

- Simplicity & Information Architecture

- Current user location within the system and the flow is unclear at certain places

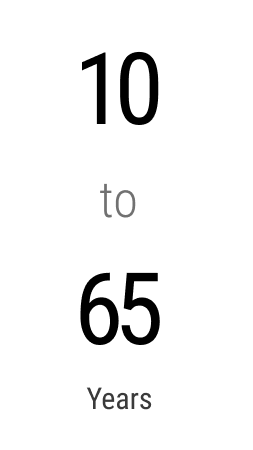

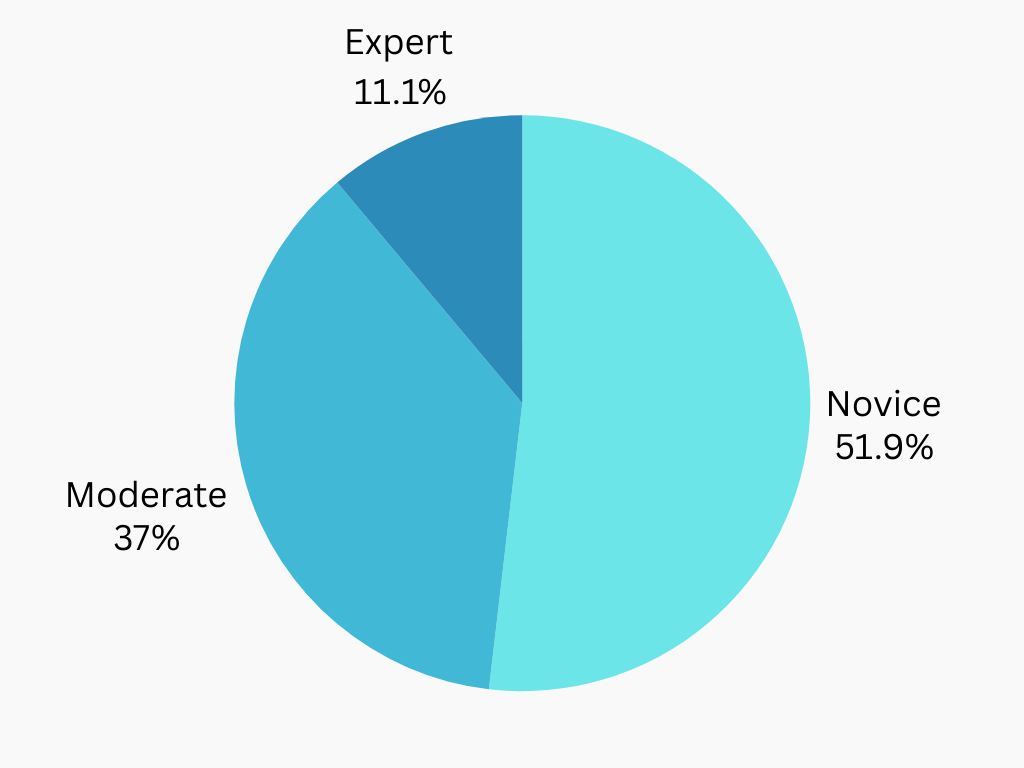

Methodology: Usability Testing with 9 users (age group b/w 10 to 65 years)

We created following set of tasks for Usability testing –

- Task 1: Set up an account

- Task 2: Create a group

- Task 3: Add an expense in the group

- Task 4: Create a reminder

- Task 5: Set a goal

- Task 6: Control access

- Task 7: Segregate expenses into personal & groups

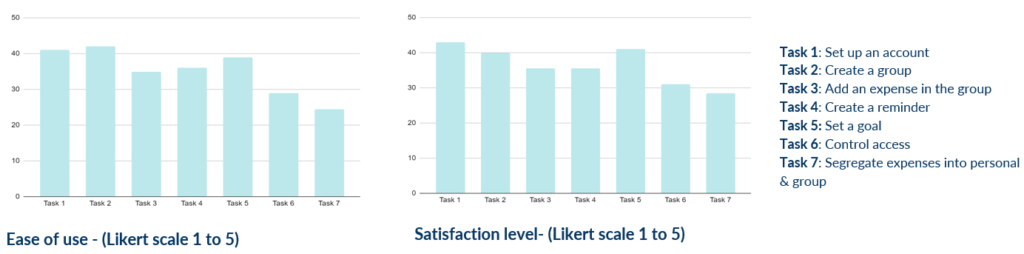

Quantitative metrics

- Task success (Yes/No)

- Level of success (First attempt, Second attempt, Third attempt, Second attempt with help)

- Ease of use (Likert scale)

- Satisfaction level (Likert scale)

Findings

Qualitative methods

- Think-out-loud technique

- Open-ended questions

Findings –

- Novice users finds it difficult to complete tasks like controlling access of group members in a group and segregating expenses into personal & group because the overall context was missing. Guided walkthrough of the app and its salient features should to be demonstrated well for them as help, especially at the very first time.

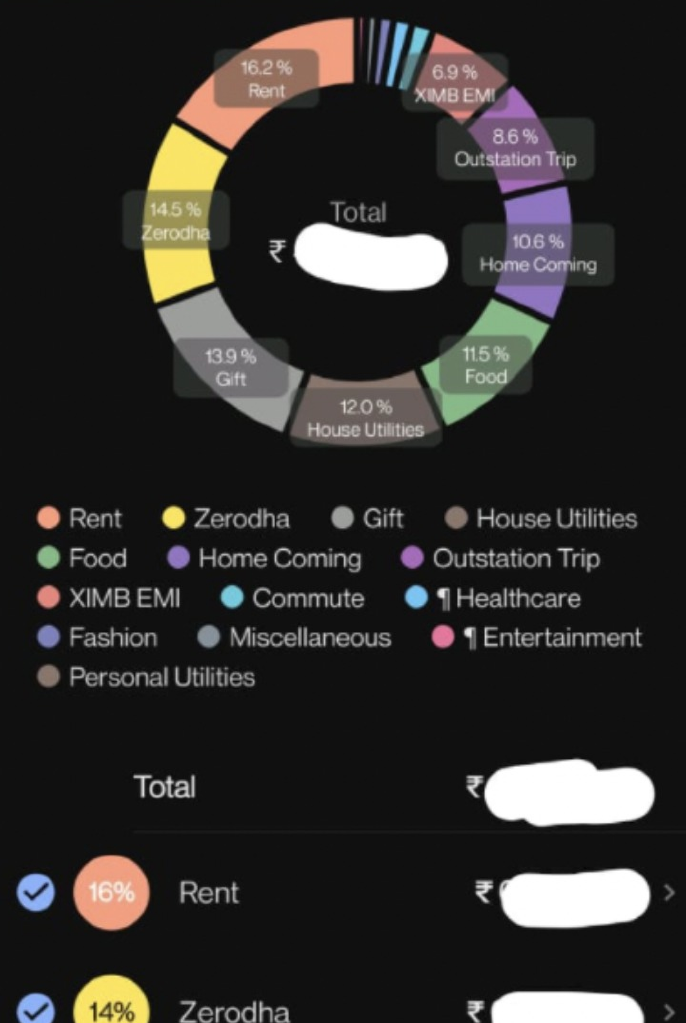

- Some of the users also faced difficulty in interpreting the data represented in the charts.

- Understanding some terminologies used in the app is another major issue. Many users didn’t understand the core context of certain terms and the CTAs were not clear.

Learnings and challenges

I worked for 6 months in this project and we never thought remote collaborations could be so much of fun. I personally started looking at things differently after this project. We learnt to conduct many of the techniques like affinity mapping, usability testing etc. remotely due to pandemic. It was not easy, but we found out new ways of doing it.

Thank you